By Erin Milburn on Monday, October 16th, 2017

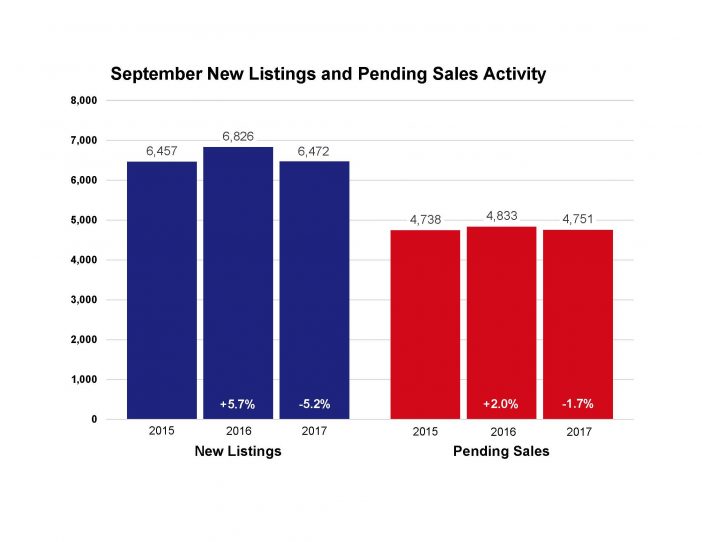

The red-hot Twin Cities housing market is starting to cool off just a bit. While June 2017 marked an all-time record for Twin Cities home sales and prices, purchase demand declined from last year for a third consecutive month. New listings decreased 5.2 percent from September 2016 to 6,472, and pending sales dipped 1.7 percent. The number of homes for sale decreased 16.7 percent to 12,502. Excluding the limited number of foreclosures and short sales, traditional new listings fell 3.6 percent while traditional pending sales increased 0.1 percent.

Since competition over limited supply remains intense, prices kept firm. The median sales price rose 7.3 percent from last year to $246,900. Home prices have now risen for the last 67 consecutive months or over 5.5 years. At 50 days on average, homes went under contract 12.3 percent faster than last September. Sellers who choose to list their properties are averaging 98.1 percent of their original list price, 0.6 percent higher than September 2016. The metro area has just 2.5 months of housing supply. Generally, five to six months of supply is considered a balanced market where neither buyers nor sellers have a clear advantage.

“There’s no other way to say it: sentiment out there may be starting to change,” said Cotty Lowry, Minneapolis Area Association of REALTORS® (MAAR) President. “Sometimes shifting markets can bring out a lot of pessimism, which can become a self-fulfilling prophecy. The likely scenario may be a brief pause in the trend we’ve seen. That’s not a bad thing, since it allows incomes a chance to catch up and takes the intensity down a notch.

”Sometimes market-wide figures mask important segment-specific realities and other indicators that buyers and sellers should be aware of. For example, closed sales only fell for homes under $250,000. Sales increased for homes priced between $250,000 and $500,000, $500,000 and $1,000,000 and for properties over $1,000,000. Market times and the ratio of sales price to list price both improved for each of the above four price ranges.

”Sometimes market-wide figures mask important segment-specific realities and other indicators that buyers and sellers should be aware of. For example, closed sales only fell for homes under $250,000. Sales increased for homes priced between $250,000 and $500,000, $500,000 and $1,000,000 and for properties over $1,000,000. Market times and the ratio of sales price to list price both improved for each of the above four price ranges.

The most recent national unemployment rate is 4.4 percent, though it’s 3.4 percent locally—the third lowest unemployment rate of any major metro area. A thriving and diverse economy has been conducive to housing recovery, as job and wage growth are key to new household formations and housing demand. The Minneapolis–St. Paul region has a resilient economy with a global reach, a talented workforce, top-notch schools, exposure to the growing technology and healthcare fields, and a quality of life that’s enabled one of the highest homeownership rates in the country.

The average 30-year fixed mortgage rate has declined from 4.3 percent to 3.8 percent recently, still well below its long-term average of around 8.0 percent. One additional rate hike may be in the cards this year, but the Fed is focused on unwinding its large portfolio. Additional inventory is still needed in order to offset declining affordability brought on by higher prices and interest rates.

“Throughout the recovery, the affordable end of the market has been the focus,” said Kath Hammerseng, MAAR President-Elect. “For homes above $250,000, the market is better supplied, less competitive and is still expanding—it’s really the bottom-end of the market that’s feeling the most inventory and therefore sales pressure.”

From The Skinny Blog.