By David Arbit on Wednesday, September 19th, 2018

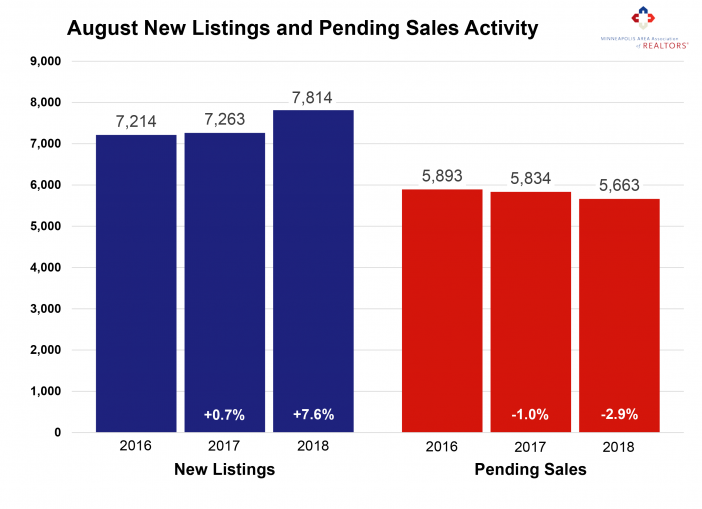

More sellers are feeling optimistic about listing their homes just as humidity, cabin weekends and food-on-a-stick give way to rakes, school buses and sweater vests. Compared to last August, Twin Cities sellers listed 7.6 percent more homes on the market. That was the largest increase since late-2015. Although buyers signed 2.9 percent fewer contracts than last year, they did manage to close on slightly more deals. Three of the last four months had increases in new listings; three of the last four months had decreases in pending sales. This trend of rising seller activity and moderating buyer activity suggests we could be approaching those long-awaited inventory gains. Sure enough, the 7.8 percent decline was the smallest decrease in inventory in over three years. Months supply was down just 3.8 percent to 2.5 months.

That said, today’s buyers still face plenty of competition over limited supply. Sellers yielded an average of 99.2 percent of their original list price and 100.1 percent of their current list price, illustrating how drastically undersupplied markets tend to favor sellers. The shortage is especially noticeable at the entry-level prices, where multiple offers and homes selling for over list price have become commonplace. The move-up and upper-bracket segments are less competitive and—for the most part—much better supplied. The market remains relatively tight, but there are some early signs that things could be loosening up for buyers.

August 2018 by the Numbers (compared to a year ago)

• Sellers listed 7,814 properties on the market, a 7.6 percent increase

• Buyers closed on 6,629 homes, a 0.2 percent increase from last August

• Inventory levels for August fell 7.8 percent compared to 2017 to 12,243 units

• Months Supply of Inventory was down 3.8 percent to 2.5 months

• The Median Sales Price rose 6.3 percent to $268,000, a record high for August

• Cumulative Days on Market declined 16.7 percent to 40 days, on average (median of 21)

• Changes in Sales activity varied by market segment

o Single family sales fell 0.8 percent; condo sales rose 15.3 percent; townhome sales increased 1.1 percent

o Traditional sales rose 1.5 percent; foreclosure sales sank 35.4 percent; short sales dropped 31.3 percent

o Previously-owned sales were down 0.5 percent; new construction sales increased 20.9 percent

From The Skinny Blog.