Thursday, June 18th, 2026

June 18, 2026

The 30-year fixed-rate mortgage decreased this week averaging 6.47%. Incoming data continues to reflect a resilient consumer, with retail sales improving and pending home sales strengthening, suggesting purchase demand is continuing to modestly improve.

- The 30-year fixed-rate mortgage averaged 6.47% as of June 18, 2026, down from last week when it averaged 6.52%. A year ago at this time, the 30-year FRM averaged 6.81%.

- The 15-year fixed-rate mortgage averaged 5.81%, down from last week when it averaged 5.84%. A year ago at this time, the 15-year FRM averaged 5.96%.

Information provided by Freddie Mac.

Posted in Interest Rates

Monday, June 15th, 2026

For Week Ending June 6, 2026

The U.S. median asking rent across the 50 largest metros dropped 1.7% from a year earlier to $1,673 in April, according to Realtor®.com, marking the 33rd consecutive month of year-over-year declines. Since peaking in August 2022, the median asking rent has declined 5.2% ($92), though it remains $254 higher than its pre-pandemic level in April 2019.

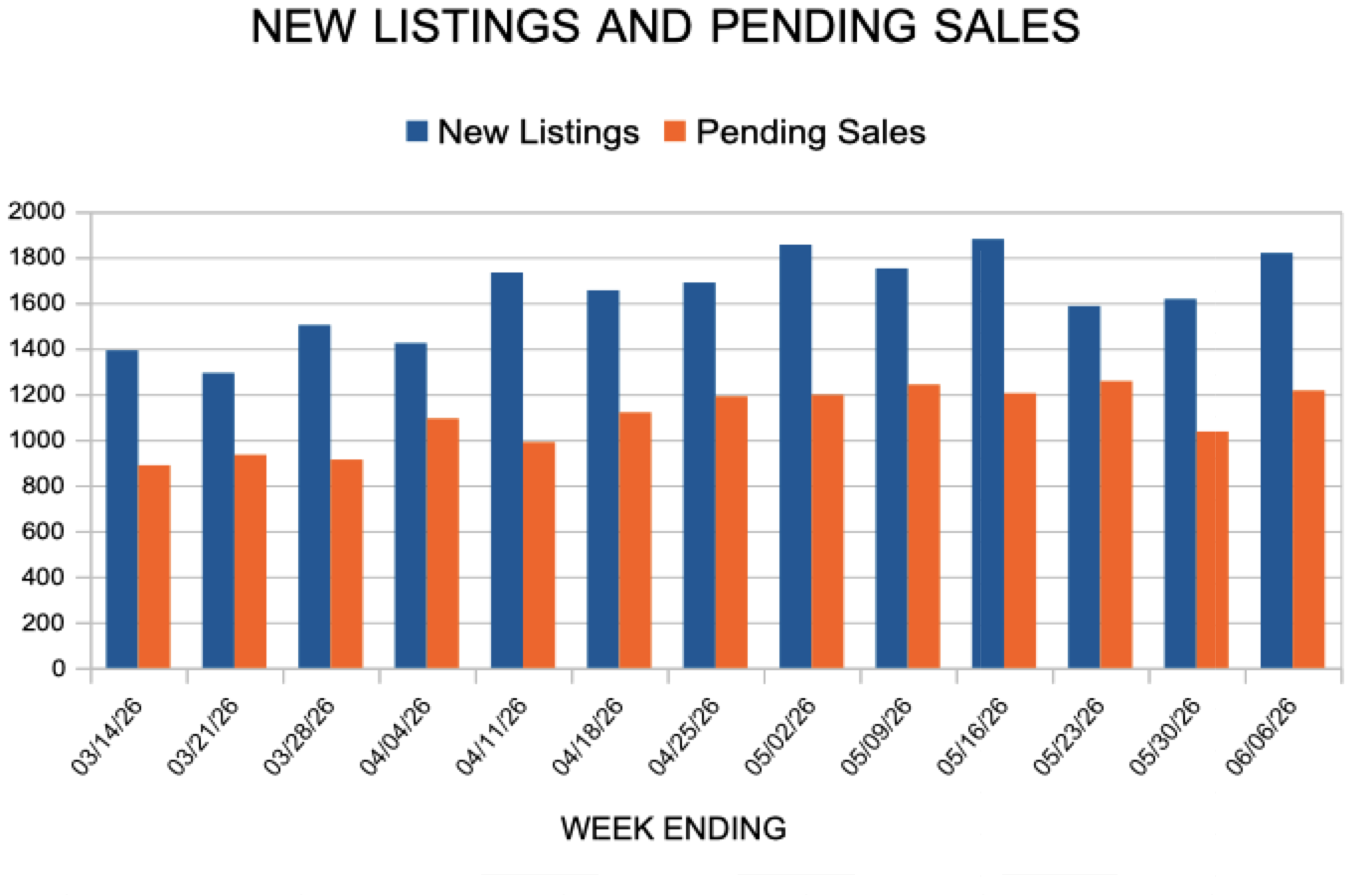

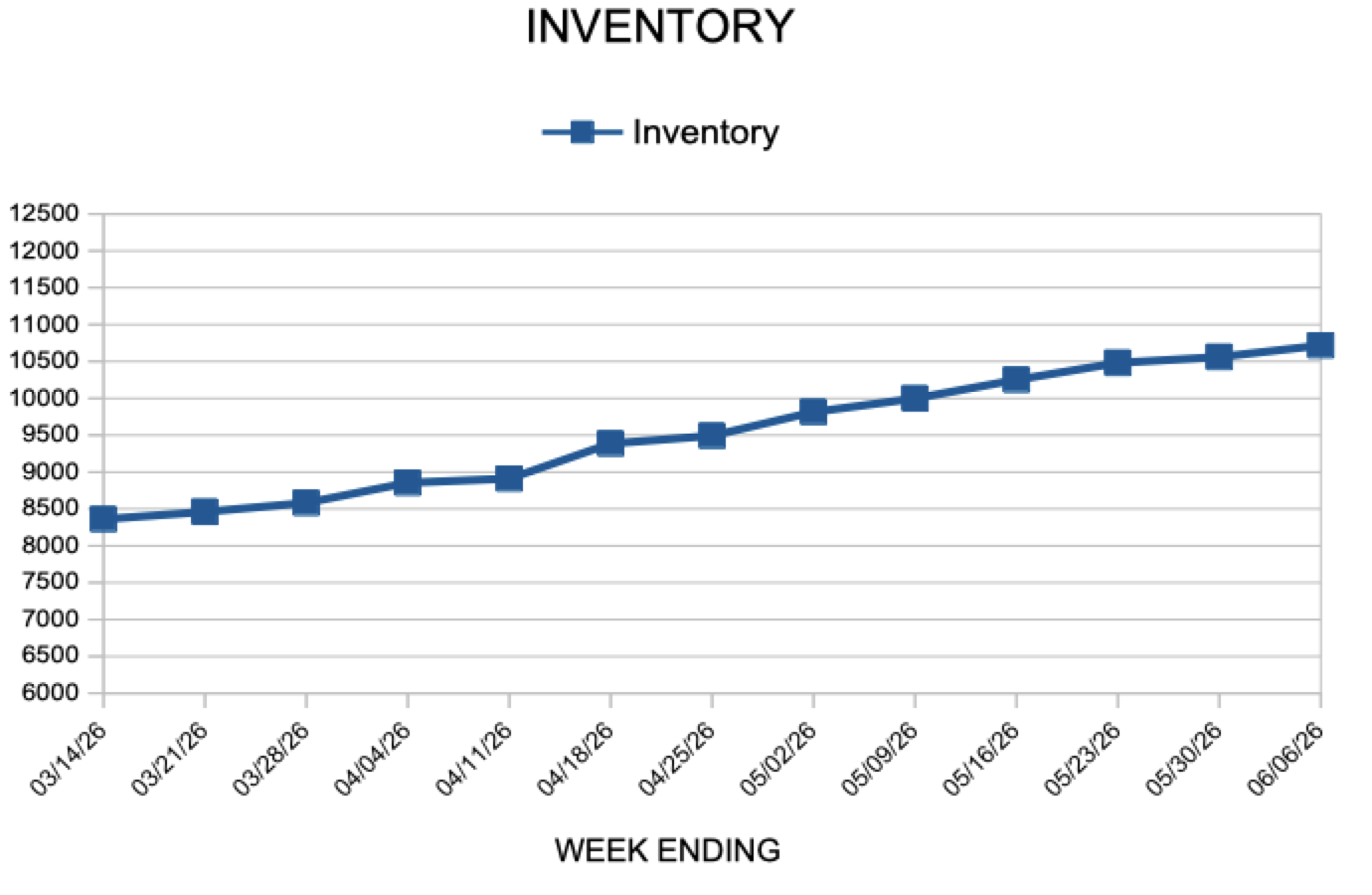

In the Twin Cities region, for the week ending June 6:

- New Listings increased 4.6% to 1,819

- Pending Sales increased 9.8% to 1,216

- Inventory increased 5.5% to 10,718

For the month of May:

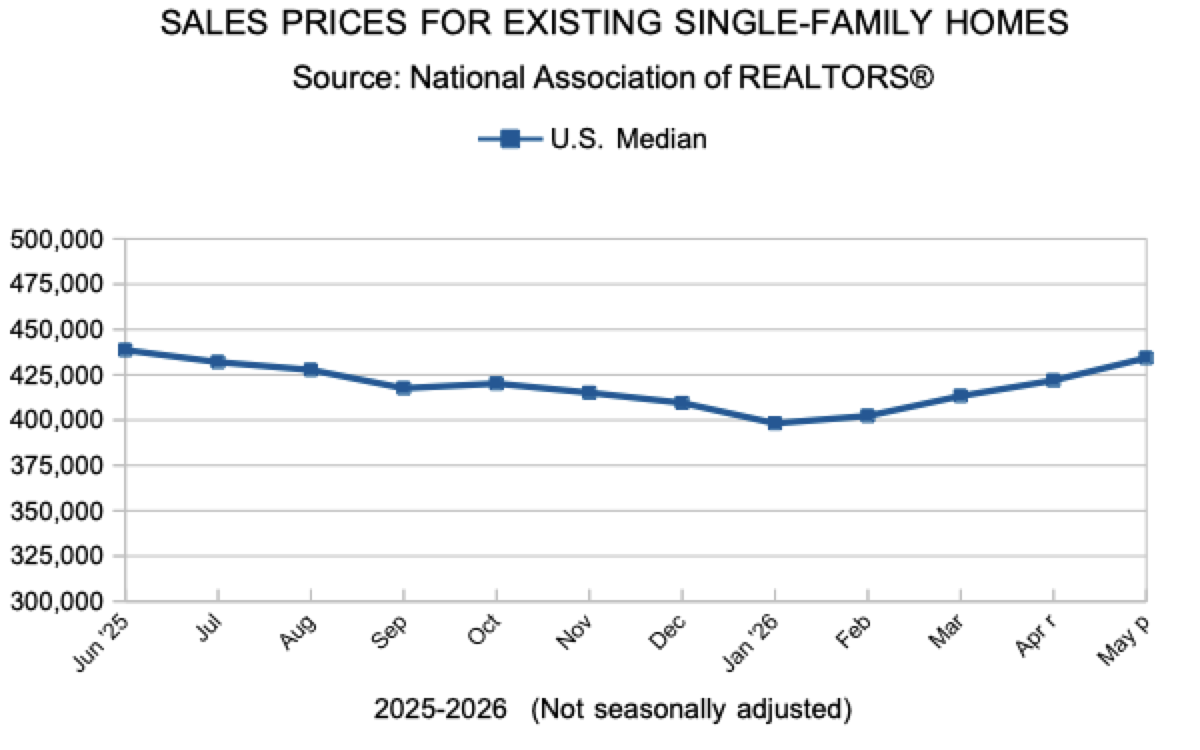

- Median Sales Price increased 1.2% to $399,900

- Days on Market increased 2.3% to 45

- Percent of Original List Price Received decreased 0.3% to 99.7%

- Months Supply of Homes For Sale increased 3.7% to 2.8

All comparisons are to 2025

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

Posted in Weekly Report